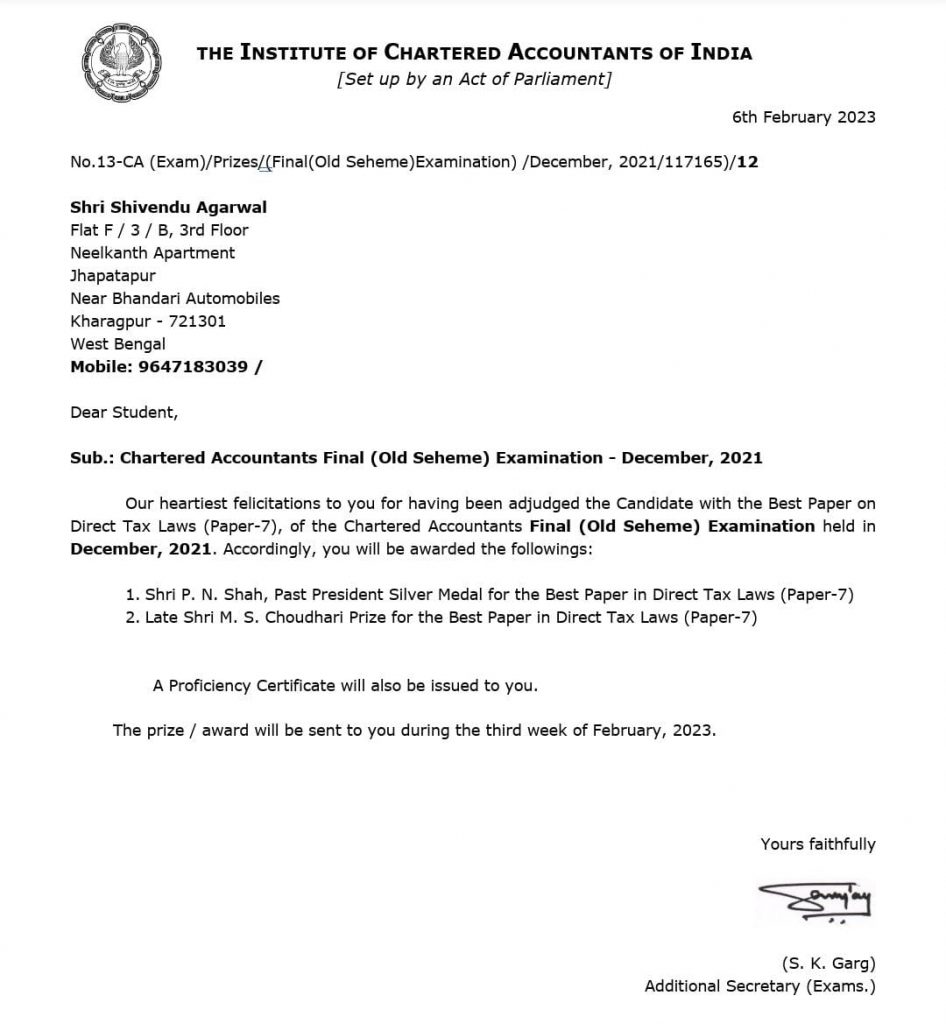

We are thrilled to announce that our partner, CA Shivendu Agarwal, has been awarded two prizes, firstly Shri P.N. Shah, Past President Silver Medal for the Best Paper in Direct Tax Laws (Paper-7) and Late Shri M.S. Choudhari Prize for the Best Paper in Direct Tax Laws (Paper-7) for his outstanding performance in the CA Final Direct Taxes Paper in the November 2021 attempt. His commendable achievement showcases his hard work, dedication, and expertise in the field of taxation.

The CA Final exams are known for their rigorous testing of candidates’ knowledge and understanding of various accounting and taxation principles. Therefore, it is a remarkable feat for CA Shivendu to receive such recognition for his exceptional performance in the Direct Taxes Paper.

Shivendu’s success is a testament to his unwavering commitment to his profession, and his ability to provide valuable insights and solutions to his clients’ complex tax-related problems. His in-depth knowledge of tax laws and regulations has enabled him to offer strategic tax planning and compliance services to clients across various industries.

As a partner of our firm, Shivendu’s expertise and dedication have played a crucial role in helping our clients navigate the ever-evolving tax landscape. His recognition as a top performer in the Direct Taxes Paper reinforces our confidence in his capabilities and reinforces our commitment to providing the best possible services to our clients.

We congratulate Shivendu on his impressive achievement and look forward to his continued success and contributions to the field of taxation. His award is a testament to his hard work, commitment, and expertise, and we are proud to have him as a partner in our firm.

Compulsory to file Income Tax Returns;- Applicable for Financial Year 2021-22 i.e. Assessment Year 2022-23. Recently, CBDT inserted a new rule 12AB which now mandates Compulsory Return Filing in all cases where following limits exceeded:-

Sales, Turnover or Gross Receipts from business exceeds INR. 60 lacs

Gross receipts from Profession exceeds INR. 10 lacs

TDS/TCS exceeds INR. 25,000 (In case of Senior Citizens INR.50,000)

Deposit in one or more Savings bank account of the person, in aggregate, is INR. 50 lacs or more

Apart from above new conditions, following other criteria already mentioned u/s 139(1) of the Income Tax Act:-

Deposited INR 1 crores or more in one or more current accounts with a banking company or co-operative bank;

Incurred expenditure of INR 2 Lacs or more on foreign travel expenses either for himself or for any other person;

Incurred expenditure of INR 1 Lacs or more towards consumption of electricity.

What are the consequences of non-filing or delay in filing of the Income Tax Returns:-

Penalty of INR. 5,000 (if filed before 31 Dec) after which penalty of INR. 10,000 will be levied.

Assessee would not be allowed to claim the benefit of certain deductions and/or set off and carry forward of losses other than loss from house property loss, due to non-filing of the tax return within the prescribed due dates.

While making an application for a loan to purchase a house/car or medical treatment or making an application for VISA of some foreign countries like the UK, US, Canada, and Australia, copy of Income Tax Return is an important document.

TDS may be deducted at double the rate applicable as per the provisions of Income Tax Return.

TDS may be deducted at double the rate applicable as per the provisions of Income Tax Return.

Interest u/s 234A at the rate of 1% pm will be levied.

Penalty u/s 270A may be levied and prosecution may also be initiated.

The above new rule 12AB is applicable for Financial Year 2021-2022 (AY 2022-23)

Whether GST rate of fly ask bricks is 5 % or 18 % as it is creating a confusion on reading of the Advance Rulling No. GUJ/GAAR/R/20/2020 Dated 02.07.2020 issued in case of Dipak Kumar Ramjibhai Patel?

The conclusion of the Advance Ruling mentioned was whether ‘Fly Ash Bricks’ manufactured and supplied by Dipakkumar Ramjibhai Patel (M/s. Mahalaxmi Cement products) are classifiable under Tariff item No.68159910 of the First Schedule to the Customs Tariff Act, 1975(51 of 1975). Applicability of GST rate on the said product would be 12% GST (6% SGST + 6% CGST) upto 14.11.2017 and 18% GST (9% SGST + 9% CGST) with effect from 15.11.2017 as per Notification No: 01/2017-Central Tax(Rate) dated 28.06.2017 (as amended from time to time) issued under the CGST Act, 2017“ means GST rate of fly ash bricks is 18% after date 15.11.2017, but we need to be more clarity based on the following discussions:

Notification No. 41/2017-Central Tax (Rate) Dated 14.11.2017 | Schedule I Sl.No. 225A | 6815 | Fly ash bricks or fly ash aggregate with 90 percent or more fly ash content” ; GST Rate – 2.50%

Notification No. 24/2018-Central Tax (Rate) Dated 31.12.2018 | Schedule I Sl.No. 225B | 6815 | Fly ash bricks or fly ash aggregate with 90 per cent or more fly a.sh content; Fly ash blocks”; GST Rate – 2.50%

REASON OF CONFUSION: Fly Ash Bricks GST rate was 12% (6% CGST + 6% SGST) vide notification 01/2017-Central Tax (Rate) Dated 28.06.2017 up to 15.11.2017 is fine in all aspects and there has no confusion.

But after amendment of the above notification vide new 41/2017-Central Tax (Rate) Dated 14.11.2017, “Fly Ash Bricks” Inserted in sl. no. 225A of Schedule-I (GST rate 5%) along with “fly ash aggregate with 90 percent or more fly ash content” under HSN 6815. The two products were clubbed together with the word “OR”, on the basis of which the AAR interpreted the line in this way that the “Fly Ash Bricks” is with 90% or more fly ash content & “Fly Ash aggregate” is also with 90% or more fly ash con-tent, which attracts GST rate 5%. But as per the industry practice and experience, Fly Ash Bricks never ever exceed the fly ash content of 70%, which is maximum. So, Fly Ash Bricks with more than 90% fly ash content does not get covered under Sl. no. 225A of notification no. 41/2017 & sl. no. 225B of 24/2018-Central Tax (Rate) Dated 31.12.2018. As the Fly Ash Bricks does not exceed Ash contains 90%, so the Authority stated that Since the ‘Fly Ash Bricks’ manufactured does not find any schedule for Fly Ash Bricks containing ash up to 60% So, the same will cover under sl.no. 453 of the notification 01/2017-Central Tax (Rate) Dated 28.06.2017 means any Chapter Goods which are not specified in Schedule I, II, IV, V or VI will attract GST rate 18%.

JUSTIFICATION FOR GST APPLICABILITY ON FLY ASH BRICKS AT 5%: On reading of the minutes of the 23rd GST Council Meeting held on date 10th November 2017, it is understood that the GST rate of Fly Ash Bricks is 5% based on the following lines collected from the council meeting papers:

AGENDA: Sl. No. 40 of Annexure-II (A) in page no. 135 shows the Rationalization of GST rates on goods [based on recommendations of the Sub-Group of Fitment Committee]:

Sl. No.

HSN

Description

Present Rate

Recommended Rate

40

6815

Fly Ash Bricks

2%

5%

Justification

GST rate on Fly ash bricks was discussed in detail in the 21st GST Council meeting.

Clay bricks attract 5% tax. Fly-ash is a pollutant.

Clay bricks are made out of top fertile soil. As against that the fly ash bricks, use fly ash a pollutant.

MINUTES OF MEETING: i) Based on the meeting discussion on Annexure II: Rationalization of GST rates on goods (based on recommendations of the Sub-Group of Fitment Committee) mentioned in page no. 19 in minutes book sl. no.19.02. :

Sl. | Recommendations

19.2 | The Honorable Minister from Odisha stated that at Sr. No.40 of Annexure II of the Agenda Notes to agenda item 6(i), the rate of tax on fly ash bricks was rightly proposed to be reduced from 12% to 5%. He suggested that fly ash aggregates, which were chip like products and consumed almost 90% of fly ash, should also be covered in this entry and should be charged to tax at the rate of 5%. Shri Tuhin Kanta Pandey, Principal Secretary (Finance), Odisha, suggested that fly ash aggregates should be classified under Chapter Heading 68 15. The Secretary suggested that rate of tax on fly ash aggregate with 90% or more fly ash content, falling under Chapter Heading 6815 may be reduced to 5%. The Council agreed to the suggestion.

ii) ln respect to the agenda item 6(i), the Council took the following decisions in minutes book sl. no.24 in page no. 24:

Sl. Council Decisions

(ii) Approve the rate of tax recommended by the Fitment Committee for goods listed in Annexure II;

(v) To reduce the rate of tax on fly ash aggregate with 90% or more fly ash content, falling under Chapter Heading 6815, from 18% to 5%.

DECISION: Sl.No. (D) (44) in page no. 18 shows the recommendations for changes in GST/IGST rate and clarifications in respect of GST rate on certain goods [As per discussions in the 23rd GST Council Meeting held on 10th November, 2017] :

Sl. No.

HSN

Description

Present Rate

Recommended Rate

44

6815

(a) Fly Ash Bricks

12%

5%

(b) Fly Ash Aggregate with 90% or more fly ash content

18%

5%

Considering all above factors of 23rd GST Council Meeting papers like Agenda, Minutes of Meetings, Decision, it clearly shows that the proposal of Honorable Minister from Odisha was duly incorporated in the Agenda paper of 23rd GST Council Meeting towards reduction of Fly Ash Bricks GST rate from 12% to 5% and accordingly it was duly noted in meetings Minutes Books and approved by the council. It was also clearly mentioned in the meeting decision paper that GST rate will be reduced from 12% to 5%.

According to the conclusion of 23rd GST Council Meeting, notification no. 41/2017-Central Tax (Rate) Dated 14.11.2017 was released by the appropriate authority showing clear intention that “Fly ash bricks or fly ash aggregate with 90 per-cent or more fly ash content” attracts GST rate 5%. Mean there are two products covered in this notification under HSN 6815 and the word “OR” is just joining to the following separate products:

1ST 6815 Fly Ash Bricks (As it can never ever cross 90%) 5.00%

2ND 6815 Fly Ash Aggregate with 90 percent or more fly ash content 5.00%

Further another 24/2018-Central Tax (Rate) Dated 31.12.2018 was released to add the 3rd product in this HSN 6815 named ” Fly ash blocks” and it also covered under the same GST rate 5%.

Moreover, we can apply principles of Interpretation of Statutes to further solidify our contention: –

We can say, interpretation of Statutes is required for two basic reasons viz. to ascertain:

• Legislative Language – Legislative language may be complicated for a layman, and hence may require interpretation; and

• Legislative Intent – The intention of legislature or Legislative intent assimilates two aspects: i the concept of ‘meaning’, i.e., what the word means; and ii. the concept of ‘purpose’ and ‘object’ or the ‘reason’ or ‘spirit’ pervading through the statute. Necessity of interpretation would arise only where the language of a statutory provision is ambiguous, not clear or where two views are possible or where the provision gives a different meaning defeating the object of the statute.

If the language is clear and unambiguous, no need of interpretation would arise.

In this regard, a Constitution Bench of five Judges of the Supreme Court in R.S. Nayak v A.R. Antulay, AIR 1984 SC 684 has held:

“… If the words of the Statute are clear and unambiguous, it is the plainest duty of the Court to give effect to the natural meaning of the words used in the provision. The question of construction arises only in the event of an ambiguity or the plain meaning of the words used in the Statute would be self defeating.” ( para 18)

The mischief rule is a rule of statutory interpretation that attempts to determine the legislator’s intention.

Originating from a 16th century case (Heydon’s case) in the United Kingdom, its main aim is to determine the “mischief and defect” that the statute in question has set out to remedy, and what ruling would effectively implement this remedy.

When the material words are capable of bearing two or more constructions the most firmly established rule or construction of such words “of all statutes in general be they penal or beneficial, restrictive or enlarging of the common law is the rule of Heydon’s case.

The rules laid down in this case are also known as Purposive Construction or Mischief Rule.

The mischief rule is a certain rule that judges can apply in statutory interpretation in order to discover Parliament’s intention. It essentially asks the question: By creating an Act of Parliament what was the “mischief” that the previous law did not cover? Heydon’s case

This was set out in Heydon’s Case [1584] 3 CO REP 7a. where it was stated that there were four points to be taken into consideration when interpreting a statute:

1. What was the common law before the making of the act?

2. What was the “mischief and defect” for which the common law did not provide?

3. What remedy the parliament hath resolved and appointed to cure the disease of the commonwealth?

4. What is the true reason of the remedy? The office of all the judges is always to make such construction as shall suppress the mischief, and advance the remedy, and to suppress subtle inventions and evasions for continuance of the mischief, and pro privato commodo, and to add force and life to the 1 7 cure and remedy, according to the true intent of the makers of the Act, pro bono publico.

The application of this rule gives the judge more discretion than the literal and the golden rule as it allows him to effectively decide on Parliament’s intent. It can be argued that this undermines Parliament’s supremacy and is undemocratic as it takes lawmaking decisions away from the legislature. Use of this Rule This rule of construction is of narrower application than the golden rule or the plain meaning rule, in that it can only be used to interpret a statute and, strictly speaking, only when the statute was passed to remedy a defect in the common law. Legislative intent is determined by examining secondary sources, such as committee reports, treatises, law review articles and corresponding statutes. This rule has often been used to resolve ambiguities in cases in which the literal rule cannot be applied.

CONCLUSION

Considering all above discussions and read together, it conclude that the intention of the Government was rightly proposed in Agenda to reduce the GST rate of HSN code 6815 99 10 from 12% to 5 % and it was duly approved by the Authority in minutes books of 23rd GST Council meeting & decision taken accordingly. Based on this decision, notification published in the portal dated 14.11.2017. So reading of “with 90 percent or more fly ash content” for both the “Fly Ash Bricks” and “Fly Ash Aggregate” is not sustainable and before “OR” is for independent product “Fly Ash Bricks” attract GST rate 5 % and after “OR” is for independent product “Fly Ash Aggregate with 90 percent or more fly ash content” attract GST rate 5 % under HSN code 9815 99 10.

Authors Note: – As per the sources and explanations in our above article, it is clear that upto 31.03.2022 the rate of GST on Fly ash bricks, with any % of fly ash content is 5%. However, as per the latest notification no. 1/2022 CT-R, dated 31st March, 2022, as applicable from 01.04.2022, the GST rate on fly ash bricks has been amended to 12% thereby clearing the entire confusion on this issue. This is a regressive step for the industry and public at large consequently increasing the cost of such items. Also, attention needs to be drawn towards notification no. 2/2022 CT-R dated 31.03.2022 and notification no. 3/2022 CT dated 31st March, 2022 and notification no. 4/2022 CT dated 31st March, 2022 wherein a concessional rate was allowed on complying with certain conditions and removing such manufacturers and traders from the benefits of Section 10 of the CGST Act, 2017.

Lok Sabha on Wednesday approved a bill to revamp the functioning of the Institute of Chartered Accountants of India (ICAI), Institute of Cost Accountants of India and Institute of Company Secretaries of India, with Union minister Nirmala Sitharaman asserting that the changes will not impact the autonomy of these bodies.

The Chartered Accountants, Cost and Works Accountants and Company Secretaries (Amendment) Bill seeks to appoint non-Chartered Accountant (CA), non-cost accountant and non-company secretary as the presiding officer of the disciplinary committees of the respective institutes.

Piloting the bill, Finance and Corporate Affairs Minister Nirmala Sitharaman said the amendments will not infringe upon the autonomy of the three institutes. Instead, it will enhance the quality of audit and improve the country’s investment climate, she added.

The amendments, she said, “will make the institutes more responsible and accountable” and encourage them to adopt global best practices. All stakeholders should have greater confidence of audit statements”.

The bill, which amends the Chartered Accountants Act, 1949, the Cost and Works Accountants Act, 1959, and the Company Secretaries Act, 1980, was later passed by the Lower House after rejecting the amendments moved by the opposition members.

Among other things, the bill provides for setting up of a coordination committee headed by the Secretary of the Ministry of Corporate Affairs. It will have representations from the three institutes.

The minister said that earlier, the three institutes had signed an MoU to set up a coordination committee but the proposal could not take off.

The committee would help in managing the resources of the institutes, she said, adding that IIMs and IITs too have coordination committees.

The bill also provides for registration of firms with the institutes and it will help in paving the way for Indian accountancy firms to grow big, she said.

It also proposes to enhance the quantum of fines for partners and firms found guilty of misconduct.

Responding to criticism that the amendments would dilute the autonomy of the institutes, the FM said, “There is no proposal or intention to impinge upon the autonomy of the three institutes. They will continue to perform their functions.”

Participating in the debate, Congress leader Adhir Ranjan Chowdhury said that while the minister referred to the US, UK, South Africa in her reply, the bill failed to abide by their best practices.

“Through this bill, the government is making a subtle and deliberate attempt to consolidate power and to snatch away the independence of institutions by dismantling the autonomous framework of the concerned institutions,” he said

NCP leader Supriya Sule said that her main concern was about the autonomy of the three reputed institutes.

“You gave the examples of IITs and IIMs. But these institutes are funded by the government while these professional institutes are not. How can they be compared? Doesn’t this take away the autonomy of these institutions?,” she asked.

RSP’s N K Premachandran also raised the issue of autonomy of these institutions.

Author Comments: This step of regularizing the disciplinary procedures for members of these institutes is a slap on the face of these institutes and raises a question mark on the integrity and honesty of these hard working professionals. This step is outrageous and is an attempt to subjugate the autonomy of these reputed institutes which have been the torch-bearers of true and fair financial reporting in the country. Mistakes do happen sometimes since these members are human after all, however, more often than not, the mistakes made by these institutes and their members are nothing compared to the “Human Errors” made by the people in sitting in power trying to monitor them, when those who are trying to monitor these institutes have been involved in “Making Mistakes” themselves. It is to be seen what the long term implications will be. Lets hope that status quo is maintained in this matter and no action is taken which may infringe upon the powers of these esteemed institutes.

We have almost reached the end of Q1 of FY 21-22 It is a testing time for all businesses across the world on account of the Coronavirus. We are all working and available to support our clients.

"We also request you to stay home and be safe"

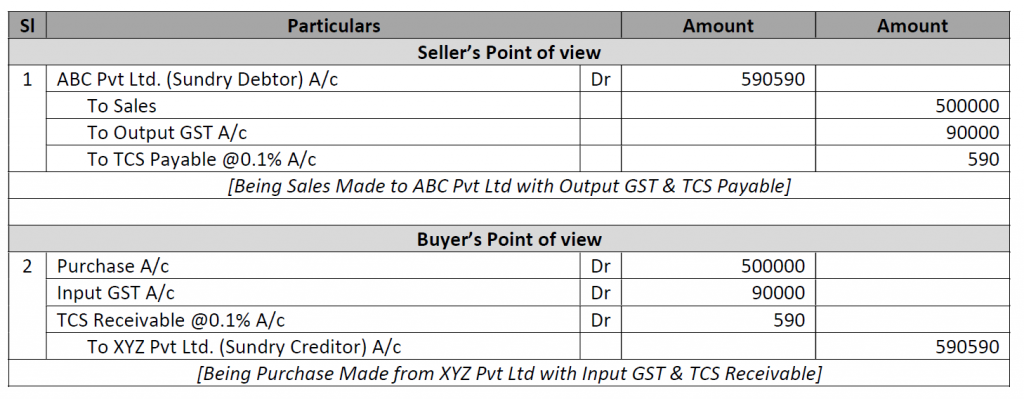

As you are aware that from 01.10.20202 TCS 206C(1H) was made effective and from 01.07.2021 TDS 194Q shall be applicable, we have summarised both the sections below along with vis-a-vis comparison & illustrations.

TCS SECTION 206C(1H)

New TCS Section 206C(1H) is made effective from 01.10.2020 vide Finance Act, 2020 and it mandates that:

A seller of goods is liable to collect TCS on sale of any goods from buyer.

TCS to be collected if the Aggregate value of goods is more than 50 lakhs.

TCS to be collected on Total sale value.

TCS @0.1% is to be collected on amount exceeding Rs. 50 lakhs if PAN of buyer is available.

If the buyer does not furnish their PAN/AADHAR number to the seller, then seller collect from the buyer, a sum equal of 1% in place of 0.1%

Seller– A person whose turnover exceeds Rs. 10 Crores in during the financial year immediately preceding, the financial year in which the sale of good is carried out. Buyer– Any person who purchase any goods, except importer of goods Central/State Government, Local Authority An embassy, High Commission, legation, commission, consulate, and trade representation of a foreign state.

ACCOUNTING JOURNAL ENTRIES

EXPLANATION A seller who receives any amount as consideration for sale of any goods. Then the Aggregate value of sale exceeding 50 lakh rupees in any previous year shall collect a sum equal to 0.1% of the sale consideration exceeding 50 lakh rupees from the buyer at the time of receipt as Income Tax. This section becomes operative from 1st October 2020.

IMPACT OF CREDIT NOTE/DEBIT NOTE If sales return/credit note/debit note is before receipt of any consideration, then the impact will be included in the amount of consideration. TCS will be applicable on the revised consideration. If the amount of consideration is already received and TCS is collected and paid, no impact will be made at the time of passing entry for sales return/credit note/debit note.

DUE DATE FOR RETURN The person responsible for collecting tax shall deposit the TCS amount within 7 days from the last day of the month in which the tax was collected. Every tax collector shall submit quarterly TCS return i.e., Form 27EQ in respect of the tax collected by him in a particular quarter.

PRACTICAL ISSUES

Issues shall arise at the end of each quarter is reconciliation. There would be some vendors who might not deposit

TCS to the government and hence the purchaser might lose the credit of such TCS.

Charging TCS becomes an issue where advances are received from customers. Since the liability of depositing TCS is on receipt of amount, TCS must be paid on such advance.

If the dates of sales and payment receipt of goods are different than TCS is applicable on receipt of sale of goods.

TCS is not applicable on Inter-Branch Stock Transfers, as PAN of both the customer and supplier is same.

FEW EXAMPLES Case – Mr. A sales goods of Rs 6000000 to Mr. B (with PAN and Aadhar detail). Solution – In case it is cover under this section and we must pay tax on 10 lakh (60 lakh – 50 lakh) and rate of tax is 0.1%. Case – Mr. A sales goods of Rs 60 lakh to Mr. B (without PAN and Aadhar detail). Solution – It is also cover under this section and taxable amount is 10 lakhs, but rate of tax is 1% because here PAN and Aadhar details are not furnished. Case – Y sales goods to Z of Rs 60 lakh. Z is liable to deduct TDS. Solution – It is not covered under this section because according to section 206C (1H) the provision of this subsection shall not apply if the buyer is liable to deduct tax at source under any other provision of this act has deducted such amount. Case – Mr. X sales goods to Mr. Y and takes advance on 29.9.2020 but sale is made on or after 1.10.2020. Solution – Receipt is before 1.10.2020, but sale is taking place after 1.10.2020, TCS should be applicable.

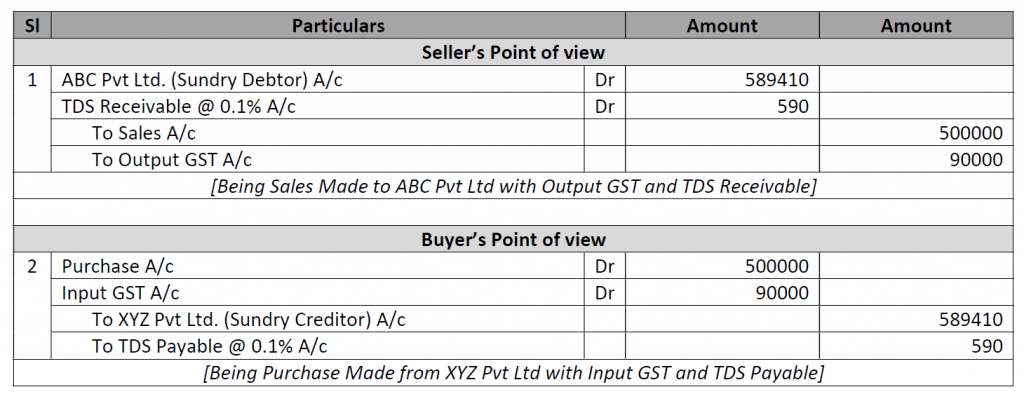

TDS SECTION 194Q

New TDS Section 194Q is made effective from 01.07.2021 vide Finance Act, 2021 and it mandates that:

Any person, being a buyer who is responsible for paying any sum to any seller for purchase of any goods.

The value or aggregate of such value exceeding fifty lakh rupees in any previous year.

Shall, at the time of credit of such sum to the account of the seller or

At the time of payment thereof by any mode, whichever is earlier,

Deduct an amount equal to 0.1 per cent. of such sum exceeding fifty lakh rupees as income-tax.

Buyer– A person whose total sales, gross receipts or turnover from the business carried on by him exceed Rs. 10 crores during the financial year immediately preceding the financial year in which the purchase of goods is carried out.

RATE OF TDS U/S 194Q Buyer of all goods will be liable to deduct tax at source @ 0.1% of sale consideration, exceeding INR 50 Lakhs in a Financial Year. Tax to be deducted @ 5% if the seller does not provide PAN/Aadhar.

TURNOVER FOR APPLICABILITY OF SECTION 194Q TDS obligation will be on buyers, whose gross receipts/turnover exceeds INR 10 Crores in preceding financial year.

ACCOUNTING JOURNAL ENTRIES

CONDITIONS FOR APPLICABILITY OF SECTION 194Q No requirement of TDS u/s 194Q on a transaction, if TDS is deductible under any other provision or TCS is collectible under section 206C excluding 206C(1H) on a given transaction. • Either TDS u/s 194Q will apply or TCS u/s 206C(1H) will apply, Both TDS u/s 194Q and TCS u/s 206C(1H) will not apply on the same transaction. • In case of potential overlap between the two provisions TDS u/s 194Q will apply and TCS u/s 206C(1H) will not apply.

DATE OF APPLICABILITY This provision will be applicable with effect from 1st July 2021. Time Limit for deduction of TDS under section 194Q Tax to be deducted at the earliest of the following dates: • Time of credit of such sum to the account of the seller or • Time of payment.

FEW EXAMPLES Case – Mr. C purchase goods of Rs 8000000 from Mr. D (with PAN detail). Solution – In case it is cover under this section and we have to deduct tax on 30 lakh (80 lakh – 50 lakh) and rate of tax is 0.1%. Case – Mr. C purchase goods of Rs 80 lakh from Mr. D (without PAN detail). Solution – It is also cover under this section and taxable amount is 30 lakh but rate of tax is 5% because here PAN details are not furnished. Case – Y purchase goods from G of Rs 70 lakh. G is liable to deduct TCS u/s 206C(1H). Solution – It will be covered under section 194Q because according to Memorandum Sec 194Q shall override Sec 206C(1H). Section 206C (1H) shall not be applicable if the buyer is liable to deduct tax at source under Sec 194Q.

Comparison of Sec 194Q and 206C(1H) of Income Tax Act, 1961

BASIS OF COMPARISON

TDS 194Q

TCS 206 (1H)

Purpose

Tax to be Deducted

Tax to be Collected

Applicable to

Buyer / Purchaser

Seller

Date of Applicability

01-07-2021

01-10-2020

When Deducted or Collected

Payment or Credit, whichever is Earlier.

At the time of Receipt.

Advances

TDS shall be deducted on advance payments made.

TCS shall be collected on advance receipts.

Rate of TDS/TCS

0.1%

0.1%

Rate if PAN Not Available

5%

1%

Exceeding Limit

Turnover/Gross Receipts/Sales from the business of buyer should exceed Rs.10 cr during previous year (excluding GST) purchase of goods of aggregate value exceeding Rs.50 lakhs in any previous year (the value of goods includes GST).

Turnover/Gross Receipts/Sales from the business of seller should exceed Rs.10 cr during previous year (excluding GST) Sale consideration received exceeds Rs.50 lakhs in any previous year. (the value of goods includes GST).

Exceptions

To be Notified by Government

If buyer is importer of goods Central/State Government, Local Authority an Embassy, High Commission, Legation, Commission, Consulate and Trade representation of a Foreign State.

When to Collect / Deposit

Tax so deducted shall be deposited with government by 7th day of subsequent month.

Tax so collected shall be deposited with government by 7th day of subsequent month.