Concept of pure agent under GST Law confuses you? Read below to get clarity.

The concept of Pure Agent and its conditions under GST Act is often a topic of confusion in the industry, particularly in cases of reimbursement of expenses. Rule 33 of CGST Rules 2017 explains that if the conditions are met, the expenditure or costs incurred by a supplier as a pure agent of the recipient of supply shall be excluded from the value of supply and will not be taxable.

The conditions for acting as a pure agent are:

(i) the supplier must act as a pure agent of the recipient of the supply and make the payment to the third party on authorization by the recipient

(ii) the payment made by the pure agent on behalf of the recipient of supply has been separately indicated in the invoice issued by the pure agent to the recipient of service

(iii) the supplies procured by the pure agent from the third party as a pure agent of the recipient of supply are in addition to the services he supplies on his own account.

Illustration- CA firm XYZ is engaged to handle the legal work pertaining to the incorporation of Company ABC Pvt. Ltd. Other than its service fees, XYZ also recovers from ABC, registration fee and approval fee for the name of the company paid to the Registrar of Companies. The fees charged by the Registrar of Companies for the registration and approval of the name are compulsorily levied on ABC. XYZ is merely acting as a pure agent in the payment of those fees. Therefore, recovery of such expenses is a disbursement and not part of the value of supply made by XYZ to ABC. “

The term “pure agent” refers to a person who enters into a contractual agreement with the recipient of supply to act as his pure agent to incur expenditure or costs in the course of supply of goods or services or both, and who neither intends to hold nor holds any title to the goods or services or both so procured or supplied as a pure agent of the recipient of supply. The pure agent should not use the goods or services so procured for his own interest, and should only recover the actual amount incurred to procure such goods or services in addition to the amount received for the supply he provides on his own account.

It is important to note that there should be a single invoice raised to the recipient for reimbursement of cost incurred and for the value of supply provided by the supplier for his/her service, and reimbursement should be separately indicated in the invoice. Also, the nature of supply procured by the pure agent from the third party as a pure agent of the recipient should be in addition to the services which he/she supplies on his own.

In cases where the applicant cannot prove that he was authorized to make the payment, or where there are two different invoices for reimbursement and for services provided by the supplier, the status of pure agent may be denied. However, if all the conditions are met, the expenditure or costs incurred by the supplier as a pure agent of the recipient of supply shall be excluded from the value of supply and will not be taxable.

So, we have dealt with main rule, we will go ahead with Explanation which deals with What is Pure Agent for purpose of

Rule 33

a. Contractual Agreement: Supplier should enter into contractual agreement with Recipient to act as Pure Agent to incur expenditure or cost

b. Ownership of Goods/Services: Pure Agent should hold or there should not be any intention to hold the Tile of Goods/Services procured as Pure Agent from third Person

c. Own Use: Pure Agent should not use the goods/services so procured for Own Use

d. Actual Amount: Pure Agent should receive the exact amount of cost/expenditure incurred in relation to procurement of goods/services, and there should not be any profit component while recovering such amount

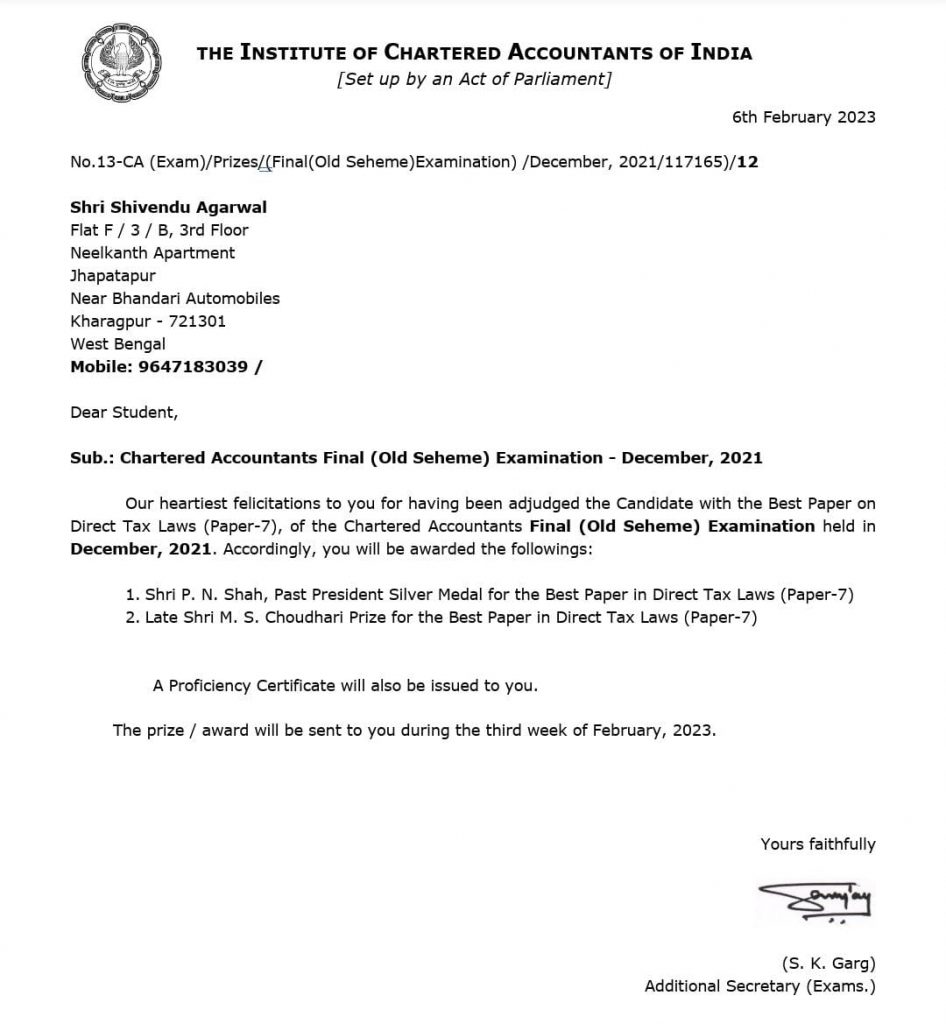

We are thrilled to announce that our partner, CA Shivendu Agarwal, has been awarded two prizes, firstly Shri P.N. Shah, Past President Silver Medal for the Best Paper in Direct Tax Laws (Paper-7) and Late Shri M.S. Choudhari Prize for the Best Paper in Direct Tax Laws (Paper-7) for his outstanding performance in the CA Final Direct Taxes Paper in the November 2021 attempt. His commendable achievement showcases his hard work, dedication, and expertise in the field of taxation.

The CA Final exams are known for their rigorous testing of candidates’ knowledge and understanding of various accounting and taxation principles. Therefore, it is a remarkable feat for CA Shivendu to receive such recognition for his exceptional performance in the Direct Taxes Paper.

Shivendu’s success is a testament to his unwavering commitment to his profession, and his ability to provide valuable insights and solutions to his clients’ complex tax-related problems. His in-depth knowledge of tax laws and regulations has enabled him to offer strategic tax planning and compliance services to clients across various industries.

As a partner of our firm, Shivendu’s expertise and dedication have played a crucial role in helping our clients navigate the ever-evolving tax landscape. His recognition as a top performer in the Direct Taxes Paper reinforces our confidence in his capabilities and reinforces our commitment to providing the best possible services to our clients.

We congratulate Shivendu on his impressive achievement and look forward to his continued success and contributions to the field of taxation. His award is a testament to his hard work, commitment, and expertise, and we are proud to have him as a partner in our firm.

CAs have a very important role in the development of our country. Moreover, the ICAI is an institute that regulates the accounting standards in India.

Chartered Accountants’ (CA) day is celebrated annually on 1 July with an aim to commemorate the findings of the Institute of Chartered Accountants of India (ICAI) by Parliament in 1949. Our Founding Partner CA Sushil Kumar Khowala, being felicitated by Jamshedpur Branch of CIRC-ICAI on occasion of 74th CA Day 2022

The ICAI is the only licensing and regulatory body for the profession of accounting and financial auditing in India. Every finance and accounting organisation including National Financial Reporting Authority (NFRA) is required to follow the recommendations of accounting standards made by them.

History

Before India became independent, the British government in India maintained accounts as per the provisions of the Companies Act. The auditor appointed for this task was expected to be certified but over the years, the designation morphed to various degrees where the accountancy profession was largely unregulated and created confusion with regards to the qualifications of auditors.

In 1948, after India got independent, an expert committee recommended that there should be a separate autonomous association of accountants to regulate their profession in the country. The Indian government accepted this recommendation and subsequently passed an act in the Parliament that led to the establishment of a statutory body named The Institute of Chartered Accountants of India (ICAI).

Significance

CAs have a very important role in the development of our country. Moreover, the ICAI is an institute that regulates the accounting standards in India.

The celebration of CA DAY is considered to be highly significant as the establishment and successful running of ICAI for all these decades has been a feat worth all the celebrations. ICAI is the world’s second-largest professional accounting body and the largest professional accounting body in India under the ownership of the Ministry of Corporate Affairs, Government of India. The first largest professional accounting body in the world is AICPA – American Institute of Certified Public Accountants.

Becoming a CA is one of the hardest career options in India. From its single-digit approval rates every year to the long and strenuous process filled with vigorous test-taking and educating practical experience (in article-ship), there are various struggles that CA aspirants need to overcome. CA Day also helps people who are on this journey or have finally completed this daunting challenge to celebrate their achievements.

The dictator-esque manner in which these innocent CAs were arrested, give GST (Good and Simple Tax) a draconian color in the eyes if the general public

In the administration of taxation, the provisions for arrests are created to tackle certain situations raised by some unscrupulous tax evaders. Arrest provisions may appear to be very harsh but these are necessary for efficient tax administration and also act as a deterrent and instill a sense of discipline. The provisions for arrests under GST Law have sufficient inbuilt safeguards to ensure that these are used only under authorization from the Commissioner. Besides this, the GST Law also stipulates that arrests can be made only in those cases where the person is involved in offences specified for the purposes of arrest and the tax amount involved in such offence is more than the specified limit.

In this regard, Section 69(1) of the Central Goods and Services Tax Act, 2017 (“the CGST Act”) reads as under:

“69. Power to arrest.

(1) Where the Commissioner has reasons to believe that a person has committed any offence specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) of section 132 which is punishable under clause (i) or (ii) of sub-section (1), or sub-section (2) of the said section, he may, by order, authorise any officer of central tax to arrest such person.”

Relevant portion of Section 132 of the CGST Act is reproduced below:

“132. Punishment for certain offences.

(1) [Whoever commits, or causes to commit and retain the benefits arising out of][1], any of the following offences, namely:-

(a) supplies any goods or services or both without issue of any invoice, in violation of the provisions of this Act or the rules made thereunder, with the intention to evade tax;

(b) issues any invoice or bill without supply of goods or services or both in violation of the provisions of this Act, or the rules made thereunder leading to wrongful availment or utilisation of input tax credit or refund of tax;

(c) avails input tax credit using the invoice or bill referred to in clause (b) or fraudulently avails input tax credit without any invoice or bill;

(d) collects any amount as tax but fails to pay the same to the Government beyond a period of three months from the date on which such payment becomes due;

shall be punishable––

(i) in cases where the amount of tax evaded or the amount of input tax credit wrongly availed or utilised or the amount of refund wrongly taken exceeds five hundred lakh rupees, with imprisonment for a term which may extend to five years and with fine;

(ii) in cases where the amount of tax evaded or the amount of input tax credit wrongly availed or utilised or the amount of refund wrongly taken exceeds two hundred lakh rupees but does not exceed five hundred lakh rupees, with imprisonment for a term which may extend to three years and with fine;

(2) Where any person convicted of an offence under this section is again convicted of an offence under this section, then, he shall be punishable for the second and for every subsequent offence with imprisonment for a term which may extend to five years and with fine.

(3) The imprisonment referred to in clauses (i), (ii) and (iii) of sub-section (1) and sub-section (2) shall, in the absence of special and adequate reasons to the contrary to be recorded in the judgment of the Court, be for a term not less than six months.

(4) Notwithstanding anything contained in the Code of Criminal Procedure, 1973, (2 of 1974) all offences under this Act, except the offences referred to in sub-section (5) shall be non-cognizable and bailable.

(5) The offences specified in clause (a) or clause (b) or clause (c) or clause (d) of sub-section (1) and punishable under clause (i) of that sub-section shall be cognizable and non-bailable.”

From a co-joint reading of the above provisions, as per Section 69 of the CGST Act, the power to arrest can only be invoked when the Commissioner having reason to believe on the basis of concrete or credentials evidence or documents and a person has committed specified offence, however, Section 132 of the CGST Act does not use the term ‘reason to believe’ and it says whoever commits or causes to commit and retains benefit from specified offences.

Thus, for arresting a CA who has simply filed GST return for a professional fee, two conditions must be met for prosecution under Section 132:

Causes to commit and

Retaining benefit

In our considered view, it cannot be said that the CA has committed an offence and professional fee cannot be said as retaining the benefit. If Section 69 wanted to arrest such tax professionals, then it should also have used the term ‘causes to commit and retains the benefit of’. Therefore, if the Commissioner wants to arrest such professionals then he has to establish that he has committed a specified offence and retained benefit which can be only established by issuance of a show cause notice and then order being passed under Section 74 of the CGST Act. At most such offence can be a bailable offence under Section 132(4) of the CGST Act.

GST Law must envisage usage of settled Law Jurisprudence by the Hon’ble SC:

SC directed for installation of CCTV Systems at investigation agencies offices and police stations

Directed for formation of State Level Oversight Committee (SLOC) and District\ Level Oversight Committee (DLOC) for purchase distribution and installation of CCTV at police stations and ensure proper working of the same. Further, directed central government to ensure that ensure that such CCTV cameras are installed at all offices of central government agencies, also where interrogation of persons takes place. This includes offices of the CBI, NIA, ED, NCB, DRI, and SFIO, etc. Stated that the Court could then summon the CCTV camera footage concerning the incident for its safekeeping. This footage may then be made available to an investigation agency to process further the complaint made to it- Hon’ble SC inParamvir Singh Saini v. Baljit Singh & Others [Special Leave Petition (Criminal) No. 3543 of 2020 dated December 02, 2020]

Guidelines required to be followed while making arrests

In a landmark judgment in the case of D.K. Basu v. State of West Bengal reported in [1997 (1) SCC 416], the Hon’ble SC has laid down specific guidelines required to be followed while making arrests. While this is in relation to police, it needs to be followed by all departments having power of arrest. These are as under:

(a) The police personnel carrying out the arrest and handling the interrogation of the arrestee should bear accurate, visible and clear identification and name tags with their designations. The particulars of all such police personnel who handle interrogation of the arrestee must be recorded in a register.

(b) The police officer carrying out the arrest shall prepare a memo of arrest at the time of arrest and such memo shall be attested by at least one witness, who may be either a member of the family of the arrestee or a respectable person of the locality from where the arrest is made. It shall also be counter signed by the arrestee and shall contain the time and date of arrest.

(c) A person who has been arrested or detained and is being held in custody in a police station or interrogation center or other lock up, shall be entitled to have one friend or relative or other person known to him or having interest in his welfare being informed, as soon as practicable, that he has been arrested and is being detained at the particular place, unless the attesting witness of the memo of arrest is himself such a friend or a relative of the arrestee.

(d) The time, place of arrest and venue of custody of an arrestee must be notified by the police where the next friend or relative of the arrestee lives outside the district or town through the Legal Aid Organization in the District and the police station of the area concerned telegraphically within a period of 8 to 12 hours after the arrest.

(e) An entry must be made in the diary at the place of detention regarding the arrest of the person which shall also disclose the name of the next friend of the person whohas been informed of the arrest and the names and particulars of the police officials in whose custody the arrestee is.

(f) The arrestee should, where he so requests, be also examined at the time of his arrest and major and minor injuries, if any present on his/her body, must be recorded at that time. The ‘Inspection Memo’ must be signed both by the arrestee and the police officer effecting the arrest and its copy provided to the arrestee.

(g) The arrestee should be subjected to medical examination by the trained doctor every 48 hours during his detention in custody by a doctor on the panel of approved doctors appointed by Director, Health Services of the concerned State or Union Territory, Director, Health Services should prepare such a panel for all Tehsils and Districts as well.

(h) Copies of all the documents including the memo of arrest, referred to above, should be sent to the Magistrate for his record.

(i) The arrestee may be permitted to meet his lawyer during interrogation, though not throughout the interrogation.

(j) A police control room should be provided at all district and State headquarters where information regarding the arrest and the place of custody of the arrestee shall be communicated by the officer causing the arrest, within 12 hours of effecting the arrest and at the police control room it should be displayed on a conspicuous notice board.

[1] Substituted vide Finance Act, 2020 dated March 27, 2020 w.e.f. January 01, 2021 before it was read as “Whoever commits any of the following offences”

Therefore, in our opinion and as per the relevant provisions of law, there are no grounds under which these innocent and young Chartered Accountants may be arrested. Moreover, the process which was followed by the CGST Department, have abused the due process of law and overridden the guidelines issued by the Hon’ble Apex Court as well. As a result, there is need to streamline these provisions in line with arrest and prosecution provisions under the Income Tax Law which have been overhauled recently.

DISCLAIMER: The views expressed are strictly of the author and SDY & CO. Chartered Accountants. The contents of this article are solely for informational purpose and for the reader’s personal non-commercial use. It does not constitute professional advice or recommendation of firm. Neither the author nor firm and its affiliates accepts any liabilities for any loss or damage of any kind arising out of any information in this article nor for any actions taken in reliance thereon. Further, no portion of our article or newsletter should be used for any purpose(s) unless authorized in writing and we reserve a legal right for any infringement on usage of our article or newsletter without prior permission.

People are slowly moving from automation to autonomous business to build an autonomous environment.

We have been hearing about automation for quite some time now, but how about moving to a future where autonomous models are at the core of the working system. Even though autonomous models are at minimum use today, it is anticipated to take over business soon. This article features why autonomous business is the future of the working systems.

Business is an umbrella term that covers initiatives in many industries. If we take the manufacturing sector into account, they have been implying automation in their working system for a long time to streamline routine tasks.

Besides manufacturing, many other industries like healthcare, banking, finance, and education are also using automation to enhance the way they function.

But the direction of the wind is changing now. People are slowly moving from automation to autonomous business to build an autonomous environment. The Covid-19 pandemic is one of the biggest events that pushed businesses to consider the autonomous way of working.

Earlier, Business Process Automation (BPA) and Business Process Management (BPM) acted as the backbone of the business. They embraced automation to improve efficiency and reduce cost.

Fortunately, the scenario has changed today. Companies are adopting autonomous business models to produce products faster, cheaper, and at a higher scale. By doing so, organizations enjoy the luxury of automating time-consuming tasks and replacing humans with machines. However, automation was the necessary ingredient that led us to autonomous business.

Some of the advantages of autonomous business are as follows

Employee productivity improvement

Employee morale is a major benefit of the autonomous business. Employees can function more effectively in a frictionless atmosphere thanks to automation.

Excellent customer support

Company processes that are automated are in a strong position to enhance customer interactions. Product or service can be made available on time. Furthermore, advances in automation such as chatbots, allow businesses to use artificial intelligence to rapidly and efficiently address customer issues, enhancing user experience.

Cost savings

There’s always a substantial waste of resources when business procedures are carried out manually. With business automation, the cost of operations is reduced and profitability is thereby increased.

Compulsory to file Income Tax Returns;- Applicable for Financial Year 2021-22 i.e. Assessment Year 2022-23. Recently, CBDT inserted a new rule 12AB which now mandates Compulsory Return Filing in all cases where following limits exceeded:-

Sales, Turnover or Gross Receipts from business exceeds INR. 60 lacs

Gross receipts from Profession exceeds INR. 10 lacs

TDS/TCS exceeds INR. 25,000 (In case of Senior Citizens INR.50,000)

Deposit in one or more Savings bank account of the person, in aggregate, is INR. 50 lacs or more

Apart from above new conditions, following other criteria already mentioned u/s 139(1) of the Income Tax Act:-

Deposited INR 1 crores or more in one or more current accounts with a banking company or co-operative bank;

Incurred expenditure of INR 2 Lacs or more on foreign travel expenses either for himself or for any other person;

Incurred expenditure of INR 1 Lacs or more towards consumption of electricity.

What are the consequences of non-filing or delay in filing of the Income Tax Returns:-

Penalty of INR. 5,000 (if filed before 31 Dec) after which penalty of INR. 10,000 will be levied.

Assessee would not be allowed to claim the benefit of certain deductions and/or set off and carry forward of losses other than loss from house property loss, due to non-filing of the tax return within the prescribed due dates.

While making an application for a loan to purchase a house/car or medical treatment or making an application for VISA of some foreign countries like the UK, US, Canada, and Australia, copy of Income Tax Return is an important document.

TDS may be deducted at double the rate applicable as per the provisions of Income Tax Return.

TDS may be deducted at double the rate applicable as per the provisions of Income Tax Return.

Interest u/s 234A at the rate of 1% pm will be levied.

Penalty u/s 270A may be levied and prosecution may also be initiated.

The above new rule 12AB is applicable for Financial Year 2021-2022 (AY 2022-23)

Whether GST rate of fly ask bricks is 5 % or 18 % as it is creating a confusion on reading of the Advance Rulling No. GUJ/GAAR/R/20/2020 Dated 02.07.2020 issued in case of Dipak Kumar Ramjibhai Patel?

The conclusion of the Advance Ruling mentioned was whether ‘Fly Ash Bricks’ manufactured and supplied by Dipakkumar Ramjibhai Patel (M/s. Mahalaxmi Cement products) are classifiable under Tariff item No.68159910 of the First Schedule to the Customs Tariff Act, 1975(51 of 1975). Applicability of GST rate on the said product would be 12% GST (6% SGST + 6% CGST) upto 14.11.2017 and 18% GST (9% SGST + 9% CGST) with effect from 15.11.2017 as per Notification No: 01/2017-Central Tax(Rate) dated 28.06.2017 (as amended from time to time) issued under the CGST Act, 2017“ means GST rate of fly ash bricks is 18% after date 15.11.2017, but we need to be more clarity based on the following discussions:

Notification No. 41/2017-Central Tax (Rate) Dated 14.11.2017 | Schedule I Sl.No. 225A | 6815 | Fly ash bricks or fly ash aggregate with 90 percent or more fly ash content” ; GST Rate – 2.50%

Notification No. 24/2018-Central Tax (Rate) Dated 31.12.2018 | Schedule I Sl.No. 225B | 6815 | Fly ash bricks or fly ash aggregate with 90 per cent or more fly a.sh content; Fly ash blocks”; GST Rate – 2.50%

REASON OF CONFUSION: Fly Ash Bricks GST rate was 12% (6% CGST + 6% SGST) vide notification 01/2017-Central Tax (Rate) Dated 28.06.2017 up to 15.11.2017 is fine in all aspects and there has no confusion.

But after amendment of the above notification vide new 41/2017-Central Tax (Rate) Dated 14.11.2017, “Fly Ash Bricks” Inserted in sl. no. 225A of Schedule-I (GST rate 5%) along with “fly ash aggregate with 90 percent or more fly ash content” under HSN 6815. The two products were clubbed together with the word “OR”, on the basis of which the AAR interpreted the line in this way that the “Fly Ash Bricks” is with 90% or more fly ash content & “Fly Ash aggregate” is also with 90% or more fly ash con-tent, which attracts GST rate 5%. But as per the industry practice and experience, Fly Ash Bricks never ever exceed the fly ash content of 70%, which is maximum. So, Fly Ash Bricks with more than 90% fly ash content does not get covered under Sl. no. 225A of notification no. 41/2017 & sl. no. 225B of 24/2018-Central Tax (Rate) Dated 31.12.2018. As the Fly Ash Bricks does not exceed Ash contains 90%, so the Authority stated that Since the ‘Fly Ash Bricks’ manufactured does not find any schedule for Fly Ash Bricks containing ash up to 60% So, the same will cover under sl.no. 453 of the notification 01/2017-Central Tax (Rate) Dated 28.06.2017 means any Chapter Goods which are not specified in Schedule I, II, IV, V or VI will attract GST rate 18%.

JUSTIFICATION FOR GST APPLICABILITY ON FLY ASH BRICKS AT 5%: On reading of the minutes of the 23rd GST Council Meeting held on date 10th November 2017, it is understood that the GST rate of Fly Ash Bricks is 5% based on the following lines collected from the council meeting papers:

AGENDA: Sl. No. 40 of Annexure-II (A) in page no. 135 shows the Rationalization of GST rates on goods [based on recommendations of the Sub-Group of Fitment Committee]:

Sl. No.

HSN

Description

Present Rate

Recommended Rate

40

6815

Fly Ash Bricks

2%

5%

Justification

GST rate on Fly ash bricks was discussed in detail in the 21st GST Council meeting.

Clay bricks attract 5% tax. Fly-ash is a pollutant.

Clay bricks are made out of top fertile soil. As against that the fly ash bricks, use fly ash a pollutant.

MINUTES OF MEETING: i) Based on the meeting discussion on Annexure II: Rationalization of GST rates on goods (based on recommendations of the Sub-Group of Fitment Committee) mentioned in page no. 19 in minutes book sl. no.19.02. :

Sl. | Recommendations

19.2 | The Honorable Minister from Odisha stated that at Sr. No.40 of Annexure II of the Agenda Notes to agenda item 6(i), the rate of tax on fly ash bricks was rightly proposed to be reduced from 12% to 5%. He suggested that fly ash aggregates, which were chip like products and consumed almost 90% of fly ash, should also be covered in this entry and should be charged to tax at the rate of 5%. Shri Tuhin Kanta Pandey, Principal Secretary (Finance), Odisha, suggested that fly ash aggregates should be classified under Chapter Heading 68 15. The Secretary suggested that rate of tax on fly ash aggregate with 90% or more fly ash content, falling under Chapter Heading 6815 may be reduced to 5%. The Council agreed to the suggestion.

ii) ln respect to the agenda item 6(i), the Council took the following decisions in minutes book sl. no.24 in page no. 24:

Sl. Council Decisions

(ii) Approve the rate of tax recommended by the Fitment Committee for goods listed in Annexure II;

(v) To reduce the rate of tax on fly ash aggregate with 90% or more fly ash content, falling under Chapter Heading 6815, from 18% to 5%.

DECISION: Sl.No. (D) (44) in page no. 18 shows the recommendations for changes in GST/IGST rate and clarifications in respect of GST rate on certain goods [As per discussions in the 23rd GST Council Meeting held on 10th November, 2017] :

Sl. No.

HSN

Description

Present Rate

Recommended Rate

44

6815

(a) Fly Ash Bricks

12%

5%

(b) Fly Ash Aggregate with 90% or more fly ash content

18%

5%

Considering all above factors of 23rd GST Council Meeting papers like Agenda, Minutes of Meetings, Decision, it clearly shows that the proposal of Honorable Minister from Odisha was duly incorporated in the Agenda paper of 23rd GST Council Meeting towards reduction of Fly Ash Bricks GST rate from 12% to 5% and accordingly it was duly noted in meetings Minutes Books and approved by the council. It was also clearly mentioned in the meeting decision paper that GST rate will be reduced from 12% to 5%.

According to the conclusion of 23rd GST Council Meeting, notification no. 41/2017-Central Tax (Rate) Dated 14.11.2017 was released by the appropriate authority showing clear intention that “Fly ash bricks or fly ash aggregate with 90 per-cent or more fly ash content” attracts GST rate 5%. Mean there are two products covered in this notification under HSN 6815 and the word “OR” is just joining to the following separate products:

1ST 6815 Fly Ash Bricks (As it can never ever cross 90%) 5.00%

2ND 6815 Fly Ash Aggregate with 90 percent or more fly ash content 5.00%

Further another 24/2018-Central Tax (Rate) Dated 31.12.2018 was released to add the 3rd product in this HSN 6815 named ” Fly ash blocks” and it also covered under the same GST rate 5%.

Moreover, we can apply principles of Interpretation of Statutes to further solidify our contention: –

We can say, interpretation of Statutes is required for two basic reasons viz. to ascertain:

• Legislative Language – Legislative language may be complicated for a layman, and hence may require interpretation; and

• Legislative Intent – The intention of legislature or Legislative intent assimilates two aspects: i the concept of ‘meaning’, i.e., what the word means; and ii. the concept of ‘purpose’ and ‘object’ or the ‘reason’ or ‘spirit’ pervading through the statute. Necessity of interpretation would arise only where the language of a statutory provision is ambiguous, not clear or where two views are possible or where the provision gives a different meaning defeating the object of the statute.

If the language is clear and unambiguous, no need of interpretation would arise.

In this regard, a Constitution Bench of five Judges of the Supreme Court in R.S. Nayak v A.R. Antulay, AIR 1984 SC 684 has held:

“… If the words of the Statute are clear and unambiguous, it is the plainest duty of the Court to give effect to the natural meaning of the words used in the provision. The question of construction arises only in the event of an ambiguity or the plain meaning of the words used in the Statute would be self defeating.” ( para 18)

The mischief rule is a rule of statutory interpretation that attempts to determine the legislator’s intention.

Originating from a 16th century case (Heydon’s case) in the United Kingdom, its main aim is to determine the “mischief and defect” that the statute in question has set out to remedy, and what ruling would effectively implement this remedy.

When the material words are capable of bearing two or more constructions the most firmly established rule or construction of such words “of all statutes in general be they penal or beneficial, restrictive or enlarging of the common law is the rule of Heydon’s case.

The rules laid down in this case are also known as Purposive Construction or Mischief Rule.

The mischief rule is a certain rule that judges can apply in statutory interpretation in order to discover Parliament’s intention. It essentially asks the question: By creating an Act of Parliament what was the “mischief” that the previous law did not cover? Heydon’s case

This was set out in Heydon’s Case [1584] 3 CO REP 7a. where it was stated that there were four points to be taken into consideration when interpreting a statute:

1. What was the common law before the making of the act?

2. What was the “mischief and defect” for which the common law did not provide?

3. What remedy the parliament hath resolved and appointed to cure the disease of the commonwealth?

4. What is the true reason of the remedy? The office of all the judges is always to make such construction as shall suppress the mischief, and advance the remedy, and to suppress subtle inventions and evasions for continuance of the mischief, and pro privato commodo, and to add force and life to the 1 7 cure and remedy, according to the true intent of the makers of the Act, pro bono publico.

The application of this rule gives the judge more discretion than the literal and the golden rule as it allows him to effectively decide on Parliament’s intent. It can be argued that this undermines Parliament’s supremacy and is undemocratic as it takes lawmaking decisions away from the legislature. Use of this Rule This rule of construction is of narrower application than the golden rule or the plain meaning rule, in that it can only be used to interpret a statute and, strictly speaking, only when the statute was passed to remedy a defect in the common law. Legislative intent is determined by examining secondary sources, such as committee reports, treatises, law review articles and corresponding statutes. This rule has often been used to resolve ambiguities in cases in which the literal rule cannot be applied.

CONCLUSION

Considering all above discussions and read together, it conclude that the intention of the Government was rightly proposed in Agenda to reduce the GST rate of HSN code 6815 99 10 from 12% to 5 % and it was duly approved by the Authority in minutes books of 23rd GST Council meeting & decision taken accordingly. Based on this decision, notification published in the portal dated 14.11.2017. So reading of “with 90 percent or more fly ash content” for both the “Fly Ash Bricks” and “Fly Ash Aggregate” is not sustainable and before “OR” is for independent product “Fly Ash Bricks” attract GST rate 5 % and after “OR” is for independent product “Fly Ash Aggregate with 90 percent or more fly ash content” attract GST rate 5 % under HSN code 9815 99 10.

Authors Note: – As per the sources and explanations in our above article, it is clear that upto 31.03.2022 the rate of GST on Fly ash bricks, with any % of fly ash content is 5%. However, as per the latest notification no. 1/2022 CT-R, dated 31st March, 2022, as applicable from 01.04.2022, the GST rate on fly ash bricks has been amended to 12% thereby clearing the entire confusion on this issue. This is a regressive step for the industry and public at large consequently increasing the cost of such items. Also, attention needs to be drawn towards notification no. 2/2022 CT-R dated 31.03.2022 and notification no. 3/2022 CT dated 31st March, 2022 and notification no. 4/2022 CT dated 31st March, 2022 wherein a concessional rate was allowed on complying with certain conditions and removing such manufacturers and traders from the benefits of Section 10 of the CGST Act, 2017.