Lok Sabha on Wednesday approved a bill to revamp the functioning of the Institute of Chartered Accountants of India (ICAI), Institute of Cost Accountants of India and Institute of Company Secretaries of India, with Union minister Nirmala Sitharaman asserting that the changes will not impact the autonomy of these bodies.

The Chartered Accountants, Cost and Works Accountants and Company Secretaries (Amendment) Bill seeks to appoint non-Chartered Accountant (CA), non-cost accountant and non-company secretary as the presiding officer of the disciplinary committees of the respective institutes.

Piloting the bill, Finance and Corporate Affairs Minister Nirmala Sitharaman said the amendments will not infringe upon the autonomy of the three institutes. Instead, it will enhance the quality of audit and improve the country’s investment climate, she added.

The amendments, she said, “will make the institutes more responsible and accountable” and encourage them to adopt global best practices. All stakeholders should have greater confidence of audit statements”.

The bill, which amends the Chartered Accountants Act, 1949, the Cost and Works Accountants Act, 1959, and the Company Secretaries Act, 1980, was later passed by the Lower House after rejecting the amendments moved by the opposition members.

Among other things, the bill provides for setting up of a coordination committee headed by the Secretary of the Ministry of Corporate Affairs. It will have representations from the three institutes.

The minister said that earlier, the three institutes had signed an MoU to set up a coordination committee but the proposal could not take off.

The committee would help in managing the resources of the institutes, she said, adding that IIMs and IITs too have coordination committees.

The bill also provides for registration of firms with the institutes and it will help in paving the way for Indian accountancy firms to grow big, she said.

It also proposes to enhance the quantum of fines for partners and firms found guilty of misconduct.

Responding to criticism that the amendments would dilute the autonomy of the institutes, the FM said, “There is no proposal or intention to impinge upon the autonomy of the three institutes. They will continue to perform their functions.”

Participating in the debate, Congress leader Adhir Ranjan Chowdhury said that while the minister referred to the US, UK, South Africa in her reply, the bill failed to abide by their best practices.

“Through this bill, the government is making a subtle and deliberate attempt to consolidate power and to snatch away the independence of institutions by dismantling the autonomous framework of the concerned institutions,” he said

NCP leader Supriya Sule said that her main concern was about the autonomy of the three reputed institutes.

“You gave the examples of IITs and IIMs. But these institutes are funded by the government while these professional institutes are not. How can they be compared? Doesn’t this take away the autonomy of these institutions?,” she asked.

RSP’s N K Premachandran also raised the issue of autonomy of these institutions.

Author Comments: This step of regularizing the disciplinary procedures for members of these institutes is a slap on the face of these institutes and raises a question mark on the integrity and honesty of these hard working professionals. This step is outrageous and is an attempt to subjugate the autonomy of these reputed institutes which have been the torch-bearers of true and fair financial reporting in the country. Mistakes do happen sometimes since these members are human after all, however, more often than not, the mistakes made by these institutes and their members are nothing compared to the “Human Errors” made by the people in sitting in power trying to monitor them, when those who are trying to monitor these institutes have been involved in “Making Mistakes” themselves. It is to be seen what the long term implications will be. Lets hope that status quo is maintained in this matter and no action is taken which may infringe upon the powers of these esteemed institutes.

Honest taxpayers & consultants bearing the brunt of Departmental misconduct and high-handedness

The Gujarat high court on Wednesday ordered an officer of the Goods and Service Tax (GST) to remain present in court on Thursday morning and bring along a tax consultant, who allegedly was in the department’s custody for the past five days without being produced before a judicial magistrate. According to petitioner Sanjay Patel, his brother Hitesh Patel, a tax consultant from Ahmedabad involved in work related to gumasta licence, was called by GST officer B D Trivedi on Friday afternoon. He claimed that, since then, the family had not been allowed to contact Hitesh. Sanjay alleged that he was permitted to give two pairs of clothes for Hitesh to a GST officer at the main gate of the GST office building on March 20, but was not allowed to meet his brother.

During the hearing, the petitioner’s advocate submitted that Hitesh had been detained on March 18, but was not produced before a magistrate. The case was mentioned before the court on Wednesday morning and the court agreed to hear it in the afternoon. Ten minutes before the hearing, the petitioner received a call from an unknown person informing him that Hitesh was being produced before the magistrate. The petitioner’s advocate contended that the GST officer’s behavior was in violation of the guidelines issued to safeguard the interest of a detainee in police custody according to two Supreme Court orders in D K Basu and Vimal Goswami cases. He argued that if the guidelines are meant for the police, the same is applicable to other agencies as well.

Summoning the GST officer, the bench of Justice Sonia GOkani and Justice Mauna Bhatt also directed him to show how guidelines laid down in the SC orders were complied with in this case.

Our View: This high-handedness by the GST Officers is the reason why courts are reprimanding Revenue Authorities wherein Principles of Natural Justice have been completely ignored and Guidelines have been violated.

The Micro, Small and Medium Enterprises(MSME) sector is a major contributor to India’s economy by way of the value it creates through manufacturing, services, exports, innovations, and employment generation. Various economic turbulences and regulatory changes have adversely affected the MSME sector, making it difficult for them to stay competitive in the domestic and global marketplace. But because of India’s strong entrepreneurial roots, this sector has sustained its growth momentum.

MSMEs contribute a whopping 30 percent to the country’s GDP and approximately 45 percent of the country’s exports. The contribution of manufacturing MSMEs in the country’s total Manufacturing Gross Value of Output has also remained constant at one-third of the total. The MSMEs and small businesses are forecasted to give employment to 16 crore Indians by 2023. The government aims to increase the MSME sector’s share in the GDP to 40 percent to benefit the rural poor, Union Minister Nitin Gadkari said, reported Business Today.

The Ministry of MSMEs is the apex executive body for the formulation, regulation and administration of rules, regulations, laws, and schemes relating to micro, small and medium enterprises in India. These enterprises need assistance and protection from large enterprises and the government as they lack resources and technology. To accomplish this, the government provides some schemes, rebates, and financial support.

The Ministry of MSMEs, by its notification that came into effect from July 1, 2020, removed any distinction between manufacturing and service sectors under the MSME definition. The following is the revised MSME classification, where the investment amount and annual turnover are similar for enterprises engaged in both sectors, aimed at bringing more SMB units under the MSME net:

Micro Enterprise: Investment less than Rs 1 crore and turnover less than Rs 5 crore

Small Enterprise: Investment less than Rs 10 crore and turnover up to Rs 50 crore

Medium Enterprise: Investment less than Rs 50 crore and turnover up to Rs 250 crore

MSME Registration Procedures

There are no separate statutes, rules and procedures for incorporating or forming MSME companies. The companies formed or incorporated under the Companies Act or other relevant Acts are eligible for registration as MSME companies, subject to certain threshold criteria as depicted above.

The registration of an MSME meeting any of the above criteria can be done through an online portal. Besides, more information on the various schemes like credit and loan schemes, subsidy schemes, etc available for MSMEs in India, can be availed here, which is the official website of the Ministry of Micro, Small and Medium Enterprises. The MSME registration process is entirely free of cost.

An Aadhaar card is mandatory for initiating the MSME registration process, along with the registered phone number.

The other documents which are required for MSME registration:

Rent agreement or ownership documents of the premises

For rented premises, NOC from the owner, rent receipts, utility bills etc

For self-owned premises, documents such as lease deed, property tax receipt

Cancelled cheque of the company

PAN Card of the company

Company registration documents

Partnership deed (if exists)

Memorandum of Association (MoA)

Articles of Association (AoA)

Copy of the Licenses and Bills of Machinery Purchased

This Guide from the MSME Ministry provides excellent information and guidelines regarding all the legal necessities and documents required for MSME registration.

To facilitate the enterprises to benefit from the various schemes, the Office of Development Commissioner (MSME) has launched a web-based application module, namely, MyMSME. This can also be accessed through a mobile app. Entrepreneurs can apply as well as track their applications on their mobiles.

Creation and Harmonious Application of Modern Processes for Increasing the Output and National Strength (CHAMPIONS) portal is a technology system for making the smaller units big by helping and hand-holding them. The portal not only helps MSMEs in the present situation but also guides them to grab new business opportunities in their growth trajectory.

Benefits of registering as MSME

Many benefits are made available by the government to the companies registered as MSME. Some of the most important and relevant benefits and schemes are discussed in the rest of this article:

1. Collateral-free bank loans under Credit Guarantee Scheme

The Government of India has facilitated the availability of collateral-free credit to all MSMEs. This initiative guarantees funds to micro and small sector enterprises without collateral. A trust named The Credit Guarantee Trust Fund Scheme was introduced by the Government of India, SIDBI (Small Industries Development Bank of India) and the Ministry of MSMEs to make the Credit Guarantee Scheme for old and new MSMEs to avail loans. The trust guarantees credit to MSMEs in place of collateral.

2. Subsidy on patent registration

MSMEs registered with the MSME ministry can avail a 50 percent subsidy on their patent registration fees. This encourages small businesses and firms to keep innovating and working on new projects and technologies, and registering patents. MSMEs and startups need to register their innovations under the Patent Act.

3. Overdraft Interest Rate Rebate

Enterprises registered as MSMEs can avail a benefit of 1 percent on the overdraft in this scheme that differs from bank to bank. This helps small businesses secure loans at lower cost and enhance their profitability.

4. Protection against delayed payments

MSMEs face the risk of delayed payments from their customers which, in turn, disturbs their entire business. Micro, Small and Medium Enterprise Development (MSMED) Act, 2006 contains provisions to deal with cases of delayed payment to micro and small enterprises. As per the provisions of the Act, the buyer is liable to pay compound interest with monthly rests to the MSME supplier on the amount at three times the bank rate notified by Reserve Bank in case they do not make payment to the supplier for the supplies of goods or services within 45 days of the day of acceptance of the goods/service or the deemed day of acceptance.

State governments are to establish Micro and Small Enterprise Facilitation Council (MSEFC) for settlement of disputes on getting references/filing on delayed payments. Every reference made to MSEFC shall be decided within ninety days from the date of making such a reference as per provisions laid in the Act.

However, there is a pitfall in this excellent rule implemented for the benefit of MSMEs in their cash flow management. The author has first-hand knowledge that many non-MSME companies hesitate to buy goods and services from MSME registered companies for the fear of enforcing the above provisions in case they delay payments.

5. Rebate on electricity bills

Another benefit the MSMEs are entitled to are concessions on their electric bill. This enables businesses to boost production and take in more orders without worrying about expenditure on costs like electricity and maintenance. They can avail of the concession by providing an application to the department of electricity along with the certificate of registration.

6. ISO certification charges reimbursement

Any registered micro, small and medium enterprise can claim reimbursement of the expenses that were made to obtain an ISO certification. This motivates entrepreneurs to get their respective businesses ISO certified which helps them to do business abroad in terms of high-quality exports.

7. Public Procurement Policy – SAMBANDH

The Ministry of MSME came with the Public Procurement Policy for Micro and Small Enterprises (MSE) with an order in 2012, later amended in 2018, which has mandated that every central ministry/department / Public Sector Units (PSU) shall set an annual goal for procurement from the MSME sector of minimum 25 percent of the total annual purchases from the products or services produced or rendered by MSEs.

A sub-target of 4 percent out of 25 percent target of annual procurement earmarked for procurement from MSEs owned by SC/ST entrepreneurs.

Special provision for micro and small enterprises owned by women. Out of the 25 percent, 3 percent shall be earmarked for procurement from MSEs owned by women.

Tender sets free of cost and exemption from payment of earnest money (EMD) to registered MSEs.

MSEs quoting price within price band L-1 + 15 percent, when L1 is from someone other than MSE, shall be allowed to supply at least 25 percent of the tendered value at L-1 subject to lowering of price by MSEs to L-1.

The implementation of Public Procurement from MSMEs is monitored through the MSME SAMBATH portal.

8. Government e-Marketplace (GeM)

GeM is a one-stop portal to facilitate online procurement of common use goods and services required by various government departments/organisations/PSUs. GeM aims to enhance transparency, efficiency, and speed in public procurement.

It provides the tools of e-bidding, reverse e-auction, and demand aggregation to facilitate the government users to achieve the best value for their money. The purchases through GeM by government users have been authorised and made mandatory by the Ministry of Finance.

9. Receivables e-Discounting System (TReDS)

Trade Receivables Discounting System (TReDS) is an electronic platform for facilitating the financing / discounting of trade receivables of MSMEs through multiple financiers. These receivables can be due from corporates and other buyers, including government departments and PSUs. It is also a cheaper alternative to banks and factoring companies.

This process involves three stakeholders; the corporate buyer, the SME supplier, and the investor/financier. The open system ensures transparency to all stakeholders and is entirely automated. It is an RBI regulated trading platform meant to buy and sell receivables on a bidding model under the payments and settlement system. An FAQ on TReds can be accessed here.

(Disclaimer: The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of SDY & Co.)

COMPANIES ON WHICH DEPOSITS CHAPTER IS NOT APPLICABLE:

Banking Company

A Non-Banking Financial Company (NBFC)

A House Finance Company (Regd with National Housing Bank)

A Government Company

PURPOSE OF THE FORM

Return of Deposit;

Particular of transaction not considered as deposits under clause (c) of Sub-rule 1 of Rule 2; or

Return of Deposit and Particulars of transactions by a company not considered as deposit.

PERIOD OF DISCLOSURE

For the financial year 2020-21 i.e. 01.04.2020 till 31.03.2021

DUE DATE

Details of particulars which are not considered as Deposits under rules; or

Reporting within 30th June of every year (details pertaining to 31st March)

NET WORTH FILING DETAILS

As given in the form itself, “Net worth as per the last audited balance sheet preceding the date of return”, which suggests, the company shall provide the details of networth of the last audited balance sheet preceeding the date of return. For example: In case the return is being filed for FY 2020-21, and the accounts for the FY 2020-21 has not been audited till the due date of the Form DPT-3, then the company shall take up the details of last audited balance sheet of the company i.e. for FY 2019-20.

CONSEQUENCES OF NON – FILING

ON THE COMPANY

Fine of minimum of Rs. 1 Crore or twice the amount of deposits whichever is lower; (Fine may extend upto Rs. 10 crore)

OFFICER IN DEFAULT

Imprisonment upto seven years and

Fine of Rs. 25 Lakhs to Rs. 2 Crore.

MANDATORY REQUIREMENT AS PER THE FORM

Auditor’s Certificate (Can only be given by the statutory auditor of the company): In case of return of Deposit, it is mandatory, where the radio button 2 or 4 is selected;

In case of any charge, Copy of Instrument creating charge;

Proof of trust deed;

Particulars of Liquid Assets;

Others, if any.

APPLICABLE FEE TO THE FORM

Nominal Share Capital

Fee Applicable

Less than Rs. 1,00,000

Rs. 200

More than Rs. 1 Lakh and less than Rs. 5 Lakh

Rs. 300

More than Rs. 5 Lakh and less than Rs. 25 Lakh

Rs. 400

More than Rs. 25 Lakh and less than Rs. 1 Crore

Rs. 500

More than Rs. 1 crore

Rs. 600

AMOUNT CONSIDERED AS EXEMPTED DEPOSITS AS PER RULE – The amount which shall not be considered as deposits has been defined under rules 2(1)(c):

Loans from Foreign Banks, Financial Institutions, IFS, etc subject to FEMA.

Money received from any company

Amount issued as Convertible Cumulative Debenture (Provided it is mandatorily converted in shares in 10 years)

Amount issued as Secured Debenture (Provided it is 100% secured)

Amount received towards subscription of any securities

Provided allotment to be made within 60 days from the date of receipt of money or advance

Amount not refunded within 15 days from completion of 60 days will be refunded as deposits. Any adjustments will not be treated as refund.

Amount raised by issuance of units

Amount received by trust (Provided no interest is paid)

Advance received for supply of goods/services (in the course of business)

Maximum 365 days

Company Law Committee recommendation to omit subject to a written contract and disclosure in financial statements.

Amount received by Directors of the company – not being borrowed fund (Relative of Director in case of private limited company also included herein)

Amount Received from employee (Amount not exceeding his/her Annual Salary)

Commercial paper in consonance with RBI guidelines

Security Deposit for performance of contract

Convertible not issued by Start-up (25 Lakh or more repayable within 5 years)

Amount received by company from AIF, MF, Domestic Capital Venture, Infrastructure trusts, Real Estate Investments Trusts.

Share Warrants

Promoters unsecured funding (on stipulation imposed by lending institution or bank)

Amount accepted by Nidhi Company

Advance received under long terms projects for supply of capital goods.

Disclosure:The entire contents of this document have been prepared on the basis of relevant provisions and as per the information existing at the time of the preparation and is of our personal opinion

We have almost reached the end of Q1 of FY 21-22 It is a testing time for all businesses across the world on account of the Coronavirus. We are all working and available to support our clients.

"We also request you to stay home and be safe"

As you are aware that from 01.10.20202 TCS 206C(1H) was made effective and from 01.07.2021 TDS 194Q shall be applicable, we have summarised both the sections below along with vis-a-vis comparison & illustrations.

TCS SECTION 206C(1H)

New TCS Section 206C(1H) is made effective from 01.10.2020 vide Finance Act, 2020 and it mandates that:

A seller of goods is liable to collect TCS on sale of any goods from buyer.

TCS to be collected if the Aggregate value of goods is more than 50 lakhs.

TCS to be collected on Total sale value.

TCS @0.1% is to be collected on amount exceeding Rs. 50 lakhs if PAN of buyer is available.

If the buyer does not furnish their PAN/AADHAR number to the seller, then seller collect from the buyer, a sum equal of 1% in place of 0.1%

Seller– A person whose turnover exceeds Rs. 10 Crores in during the financial year immediately preceding, the financial year in which the sale of good is carried out. Buyer– Any person who purchase any goods, except importer of goods Central/State Government, Local Authority An embassy, High Commission, legation, commission, consulate, and trade representation of a foreign state.

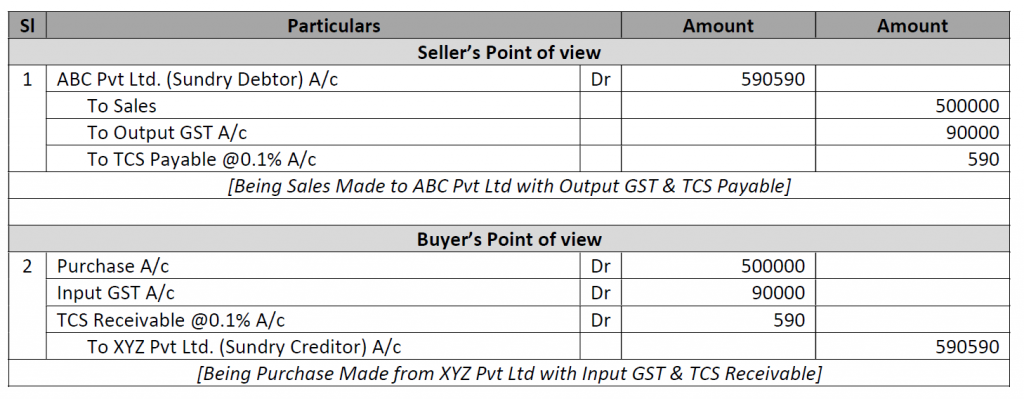

ACCOUNTING JOURNAL ENTRIES

EXPLANATION A seller who receives any amount as consideration for sale of any goods. Then the Aggregate value of sale exceeding 50 lakh rupees in any previous year shall collect a sum equal to 0.1% of the sale consideration exceeding 50 lakh rupees from the buyer at the time of receipt as Income Tax. This section becomes operative from 1st October 2020.

IMPACT OF CREDIT NOTE/DEBIT NOTE If sales return/credit note/debit note is before receipt of any consideration, then the impact will be included in the amount of consideration. TCS will be applicable on the revised consideration. If the amount of consideration is already received and TCS is collected and paid, no impact will be made at the time of passing entry for sales return/credit note/debit note.

DUE DATE FOR RETURN The person responsible for collecting tax shall deposit the TCS amount within 7 days from the last day of the month in which the tax was collected. Every tax collector shall submit quarterly TCS return i.e., Form 27EQ in respect of the tax collected by him in a particular quarter.

PRACTICAL ISSUES

Issues shall arise at the end of each quarter is reconciliation. There would be some vendors who might not deposit

TCS to the government and hence the purchaser might lose the credit of such TCS.

Charging TCS becomes an issue where advances are received from customers. Since the liability of depositing TCS is on receipt of amount, TCS must be paid on such advance.

If the dates of sales and payment receipt of goods are different than TCS is applicable on receipt of sale of goods.

TCS is not applicable on Inter-Branch Stock Transfers, as PAN of both the customer and supplier is same.

FEW EXAMPLES Case – Mr. A sales goods of Rs 6000000 to Mr. B (with PAN and Aadhar detail). Solution – In case it is cover under this section and we must pay tax on 10 lakh (60 lakh – 50 lakh) and rate of tax is 0.1%. Case – Mr. A sales goods of Rs 60 lakh to Mr. B (without PAN and Aadhar detail). Solution – It is also cover under this section and taxable amount is 10 lakhs, but rate of tax is 1% because here PAN and Aadhar details are not furnished. Case – Y sales goods to Z of Rs 60 lakh. Z is liable to deduct TDS. Solution – It is not covered under this section because according to section 206C (1H) the provision of this subsection shall not apply if the buyer is liable to deduct tax at source under any other provision of this act has deducted such amount. Case – Mr. X sales goods to Mr. Y and takes advance on 29.9.2020 but sale is made on or after 1.10.2020. Solution – Receipt is before 1.10.2020, but sale is taking place after 1.10.2020, TCS should be applicable.

TDS SECTION 194Q

New TDS Section 194Q is made effective from 01.07.2021 vide Finance Act, 2021 and it mandates that:

Any person, being a buyer who is responsible for paying any sum to any seller for purchase of any goods.

The value or aggregate of such value exceeding fifty lakh rupees in any previous year.

Shall, at the time of credit of such sum to the account of the seller or

At the time of payment thereof by any mode, whichever is earlier,

Deduct an amount equal to 0.1 per cent. of such sum exceeding fifty lakh rupees as income-tax.

Buyer– A person whose total sales, gross receipts or turnover from the business carried on by him exceed Rs. 10 crores during the financial year immediately preceding the financial year in which the purchase of goods is carried out.

RATE OF TDS U/S 194Q Buyer of all goods will be liable to deduct tax at source @ 0.1% of sale consideration, exceeding INR 50 Lakhs in a Financial Year. Tax to be deducted @ 5% if the seller does not provide PAN/Aadhar.

TURNOVER FOR APPLICABILITY OF SECTION 194Q TDS obligation will be on buyers, whose gross receipts/turnover exceeds INR 10 Crores in preceding financial year.

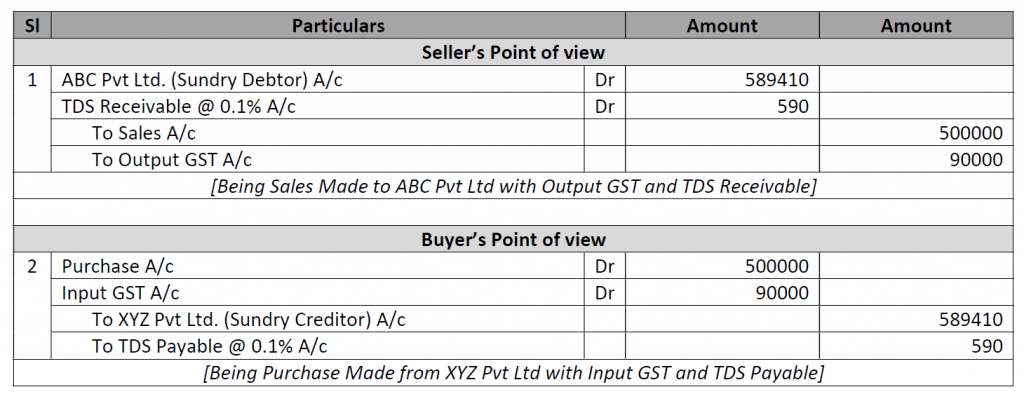

ACCOUNTING JOURNAL ENTRIES

CONDITIONS FOR APPLICABILITY OF SECTION 194Q No requirement of TDS u/s 194Q on a transaction, if TDS is deductible under any other provision or TCS is collectible under section 206C excluding 206C(1H) on a given transaction. • Either TDS u/s 194Q will apply or TCS u/s 206C(1H) will apply, Both TDS u/s 194Q and TCS u/s 206C(1H) will not apply on the same transaction. • In case of potential overlap between the two provisions TDS u/s 194Q will apply and TCS u/s 206C(1H) will not apply.

DATE OF APPLICABILITY This provision will be applicable with effect from 1st July 2021. Time Limit for deduction of TDS under section 194Q Tax to be deducted at the earliest of the following dates: • Time of credit of such sum to the account of the seller or • Time of payment.

FEW EXAMPLES Case – Mr. C purchase goods of Rs 8000000 from Mr. D (with PAN detail). Solution – In case it is cover under this section and we have to deduct tax on 30 lakh (80 lakh – 50 lakh) and rate of tax is 0.1%. Case – Mr. C purchase goods of Rs 80 lakh from Mr. D (without PAN detail). Solution – It is also cover under this section and taxable amount is 30 lakh but rate of tax is 5% because here PAN details are not furnished. Case – Y purchase goods from G of Rs 70 lakh. G is liable to deduct TCS u/s 206C(1H). Solution – It will be covered under section 194Q because according to Memorandum Sec 194Q shall override Sec 206C(1H). Section 206C (1H) shall not be applicable if the buyer is liable to deduct tax at source under Sec 194Q.

Comparison of Sec 194Q and 206C(1H) of Income Tax Act, 1961

BASIS OF COMPARISON

TDS 194Q

TCS 206 (1H)

Purpose

Tax to be Deducted

Tax to be Collected

Applicable to

Buyer / Purchaser

Seller

Date of Applicability

01-07-2021

01-10-2020

When Deducted or Collected

Payment or Credit, whichever is Earlier.

At the time of Receipt.

Advances

TDS shall be deducted on advance payments made.

TCS shall be collected on advance receipts.

Rate of TDS/TCS

0.1%

0.1%

Rate if PAN Not Available

5%

1%

Exceeding Limit

Turnover/Gross Receipts/Sales from the business of buyer should exceed Rs.10 cr during previous year (excluding GST) purchase of goods of aggregate value exceeding Rs.50 lakhs in any previous year (the value of goods includes GST).

Turnover/Gross Receipts/Sales from the business of seller should exceed Rs.10 cr during previous year (excluding GST) Sale consideration received exceeds Rs.50 lakhs in any previous year. (the value of goods includes GST).

Exceptions

To be Notified by Government

If buyer is importer of goods Central/State Government, Local Authority an Embassy, High Commission, Legation, Commission, Consulate and Trade representation of a Foreign State.

When to Collect / Deposit

Tax so deducted shall be deposited with government by 7th day of subsequent month.

Tax so collected shall be deposited with government by 7th day of subsequent month.